|

By the end of this lesson you'll have learned:

Why should I care? Even if you don’t think you have an immediate need for a stellar credit score, it can impact your life more than you may realize. Here are a few things your credit score can affect:

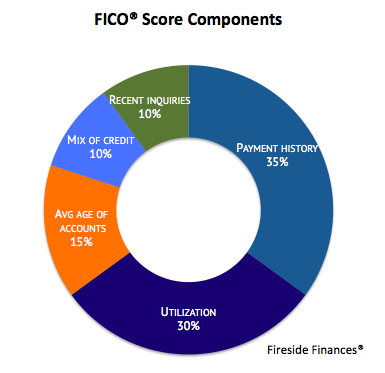

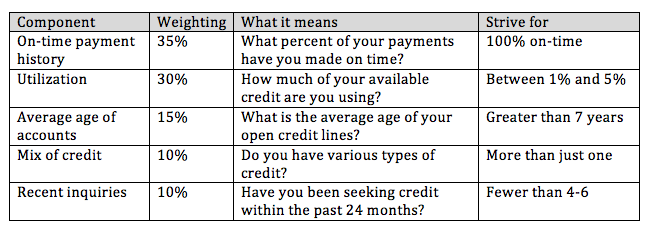

What are the best (and free) ways to check my credit score? My two favorite apps are CreditKarma and Experian. Both are free and I check them on my phone a few times per month. I highly recommend installing them and allowing push notifications so you can be alerted to any changes to your credit report. Experian has a few paid options that I mention in more detail below, but the basic service is great as it is. (Note that CreditKarma doesn’t provide your true FICO® score, but rather a score based on a model called VantageScore 4.0.) Most banks now provide your actual FICO® score for free Bank of America, Discover, American Express, Wells Fargo, Chase, USAA, Barclays, and US Bank all provide your actual FICO®. Simply log in and poke around your web interface until you find it. Many will even give you a graph of how it has trended over time. Even if you don't have a credit card, Discover lets you see your FICO® score for free; pretty sweet. Now that you have your score in hand, let’s talk about why it’s important. The difference between a top credit score and a poor credit score can literally change your mortgage rate by several hundred dollars per month, depending on the size of the loan of course. That’s why it’s worth investing a few hours of your time now, even if it’s years before you are ready to buy a home. How credit scores are calculated To understand how to boost your score let’s first take a look at scores are calculated. There are five components with various weightings:

Utilization - the magic lever

We could spend quite a bit of time on each of these, but I want to focus on Utilization. The ratio of credit you are using to the total credit you have available, typically expressed as a percentage, is called utilization. It is the only one of the five components that has no history. Meaning, it could be 80% this month and if you lower it to 10% next month, your updated score is based on 10%. Because of the fact it has no history and also because it accounts for the second-largest percentage of your score, I find this component the easiest one to tweak to increase your score. We’ll use my coworker Bill as an example (true story!) I gave a talk about credit scores and Bill was able to boost his score in just two months by lowering his utilization. Bill had $5,000 of available credit with only one open card. In a typical month he charged $2,000 worth of expenses and paid it all off (accrued no interest.) His utilization was calculated as: $2,000 / $5,000 = 40% If you are like Bill and have a utilization above about 10%, applying for a new card or raising your existing credit limit, can actually help your score. It may seem counterintuitive, but take a look how it may help. Bill applied for a new Chase card and was granted a $15,000 credit line. He then had a total of $20,000 of available credit across two cards. Assuming he maintains his typical expenses of $2,000, his new overall utilization was: $2,000 / $20,000 = 10% He decreased his utilization from 40% to 10% by adding another card. That was a pretty significant drop, and he got himself under the key 30% threshold that is often referenced. 40% to 10% will obviously have a bigger impact than lowering your utilization from say 4% to 3%. (Another way to lower your utilization is to make a mid-cycle payment to your account, so when the statement closes the balance is lower.) It should go without saying, but I’ll mention it just in case. If the additional credit will tempt you spend more, it’s not a smart idea to get more credit! Also note that you can expect your score to drop about 5 points for the initial hit of applying for a new card. But as you can see from the table above, utilization accounts for 30% of your score while recent inquiries account for only 10%. The temporary drop should fade away in 2-3 months and you should see a boost when the additional utilization is reported. You want to keep your overall utilization low as well as your per card utilization. If one card has only a $500 limit, don’t put $400 on that one. Some issuers will increase your credit limit without a hard pull (defined below), or will let you re-allocate your credit if you have several cards with them. (For example, I have several Chase cards. Before I close one out, I re-allocate my credit line on that card to another Chase card that I plan to leave open, thereby protecting my utilization.) Other Credit Tips: There are many more important aspects of your credit score to learn about, which we will go over in future lessons. In the meantime, here are 5 other tips I’ve curated over the years:

Some of my favorite no-annual-fee credit cards: Chase Freedom Unlimited: 1.5% cash back on everything. Especially powerful when combined with the Chase Sapphire Reserve; then it’s 2.25% back on everything. American Express Blue Business Plus: 2% cash back on everything, but not everywhere takes Amex so it's good to have a backup card. (Personally, I use this card and redeem Membership Rewards points through my Amex Schwab Platinum to get a net 2.5% cash back on all purchases. Military readers take note: Amex has a generous interpretation of the SCRA and graciously waives annual fees for all their cards, including all flavors in the Platinum lineup!) Reminder that Fireside Finances does not use referral or affiliate links. We always put you, the reader, first, and never want to give the impression we are recommending a card, account, or product for our financial gain. There are referral bonuses for the two above cards, so if you are feeling generous, find someone who holds that card and make them an extra $100! Fireside Fable A friend of mine (let’s call her Alicia) unfortunately missed a payment to her credit card and dinged her perfect record of 100% of payments on-time. Doh! To avoid this, I recommend two things:

Let’s get back to Alicia. She needs to minimize the damage her missed payment made on her score. CreditKarma will tell you the number of total payments on your credit report. Let’s say Alicia has 75 total payments, 1 of which was late. Her % of on-time payments is now 74/75 = 98.7%. Not bad, but not 100% either. I explained to Alicia that she could “dilute” the effect of the missed payment by making on-time payments on her other cards each month. It doesn’t matter the size of the payment, $5 or $5,000, it’s still one on-time payment. It’s a long play, but by making more on-time payments you are increasing the denominator of that ratio more rapidly, minimizing the effect of the missed payment. This works well if you have several dormant cards that you normally don’t use.

1 Comment

|

All information contained within is provided for educational purposes only and should not be interpreted as financial advice. Readers are encouraged to speak with their financial professional or tax professional. Fireside Finances, LLC does not provide tax advice. Past performance is not a guarantee of future results. Fireside Finances, LLC does not receive compensation or affiliate revenue from any of the companies referenced on the site.

Fireside Finances, LLC is a registered investment adviser in the State of California. The Adviser may not transact business in states where it is not appropriately registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

ADV Part 2A | Privacy Policy

Fireside Finances, LLC is a registered investment adviser in the State of California. The Adviser may not transact business in states where it is not appropriately registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

ADV Part 2A | Privacy Policy