LEVEL FOUR / I'M AN ACADEMY CADET!

Lesson 2: Cadet Roth IRA

By the end of this lesson, you'll have learned: 1) Roth IRA limits, 2) where to open a Roth IRA, 3) how to invest your Roth IRA, 4) how to designate a beneficiary.

introduction

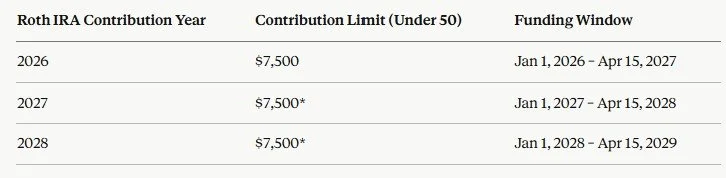

Roth IRA’s are arguably the best way to save for your retirement. You pay your tax now and then do not pay taxes in the future. In fact, the Roth IRA is such a “great deal” the IRS only allows single individuals earning <$153k / year in 2026 to contribute. (Fidelity) Perhaps they figure that higher earners do not need the tax break. One can contribute to a Roth IRA provided he or she has earned income for the year. Fortunately, all cadets have well over $7,500 of earned income, even though they don’t actually receive that much in their checking account each year. While technically one can take out Roth IRA contributions (not earnings) at any time without a penalty, it's best to think of your investment in a Roth IRA as money you won't touch or need until 59.5 years old.

* The 2027 & 2028 Roth IRA Contribution Limits have not yet been announced, so check back later when those numbers are released. The limit typically increases by $500 every other year or so, depending on inflation. Also, people over 50 years of age are allowed an additional $1,100 per year catch-up contribution as of 2026.)

Mechanically, contributing to a Roth IRA is quite easy. I opened one in 4 minutes at Vanguard.com.

Here are your steps:

Open the account

Link your bank account (USAA, Marcus, etc.)

Fund your Roth IRA by initiating the transfer at Vanguard

Select which year you want the contribution to apply to (max the earliest year first, provided you have earned income to support it.)

Invest the cash

Designate an account beneficiary (sibling, parent, charity)

why do you recommend vanguard for my roth ira?

I like Vanguard because they are owned by their members, similar to a co-op. Their fees are among the lowest in the industry and any profits they make are returned to their investors through a reduction in fund costs. I also really identify with their company values. In fact, one of the main reasons I became a CFP® professional is because I firmly believe in doing what's best for the client (holding the fiduciary standard). (See my Fireside Fable below for a fun story on Vanguard.)

A quick reminder: I don’t have any affiliate or referral relationships with any of these financial institutions. I only recommend companies I use personally and think highly of. There are many places you could open your Roth IRA: Vanguard, Fidelity, Schwab, USAA, NFCU, Betterment, or Wealthfront, to name a few. Personally, I love Vanguard and their low-fee target date funds. I also love Fidelity because their customer service is terrific, many civilian employers use them for 401(k)s, and they have branches (Investor Centers) in most major cities. I use USAA for banking and insurance, and Vanguard, Fidelity, and the TSP for investing. But don’t obsess over where to open your Roth IRA, just open it! I've seen some folks hit decision paralysis because they feel the need to deeply research the pros and cons of each company, only to be two years down the road and they still haven't made a decision. Seriously, just get your Roth IRA going, even if that means walking down the hill and opening it at the Navy Federal branch. You can always move it later without tax consequence if done properly.

what should i do with the cash once it’s in my roth ira?

Now that you’ve made your contribution, you have to select an investment. This is a personal choice, but I’m a firm believer in demanding market returns for the risk you take. I believe in broadly diversified funds with low expenses, such as Vanguard’s Target Date Funds. If I were ~20 years old, I'd invest in VSVNX, Vanguard’s 2070 Target Date Fund, which is 90% stocks and 10% bonds. Just know that this is a 40+ year investment and market fluctuations are very normal. There’s a strong possibility your account balance could decrease over the next few years and that’s perfectly okay. Hang on for the ride and view the market dips as buying opportunities! Target Date Funds are nice because not only are they inexpensive (0.08% at Vanguard) and they also rebalance automatically every year. This means your investment will get more conservative each year you approach your retirement year, which reduces the risk in your portfolio. They are designed to be “set it and forget it” funds.

setting a beneficiary

As you grow your wealth you’ll want to ensure it goes to the people/places you care about in the event you pass away. Designating a beneficiary is very important, but sadly many folks gloss right over this step, or don’t review it after a life event. You can designate a sibling, parent, friend, or even a charity. You can also set a “contingent beneficiary” in the event you and your beneficiary die together. (For example, I’ve set my beneficiary as my wife on all of my accounts. However, my wife and I often travel together, so it’s possible something could happen to us both at the same time. Therefore I’ve set my brother as my contingent beneficiary.) You can always update your beneficiary after you get married. Also make a mental note to designate a beneficiary for your TSP when you open one as an Ensign.

Ask your parents for a Roth IRA match

Try asking your parents for a Roth IRA match. Could go something like this… “Mom/Dad, I’d like to get a jump start on saving for retirement by opening a Roth IRA. I’d like to max it out but am not sure I’ll have the full amount. Would you consider matching my savings?” Perhaps you can each contribute $3,750. Obviously this greatly depends on your family situation and where your parents are financially. Many parents would recognize the value and willingly contribute, proud of their kids for taking the reins on their retirement savings at such a young age. Other parents may laugh their kids out of the room. I’ll let you decide if you should raise the point about them not having to pay for college :)

FIRESIDE FABLE

After my time on active duty I went to San Francisco and worked for a fintech startup called FutureAdvisor. It was an awesome job and working for a startup with 25 people felt completely opposite from working for a 45,000 person governmental organization. After about a year of working at FutureAdvisor, it was announced at a surprise all-hands the company was being acquired by BlackRock -- lucky us! (BlackRock is the world's largest asset manager, responsible for over $6 trillion dollars, including many TSP funds and some of Vanguard's fixed income funds too.) I'll never forget, they announced the acquisition to us at 1:01pm Pacific Time, exactly after the NYSE closed for the day (4:00pm Eastern Time). A press release would be issued before the market opened the next morning we were told. This was done on purpose, so we wouldn't be in receipt of non-public information while the market was open. Smart.

There was a lot of fanfare after the acquisition, including some really fun parties with senior BlackRock executives. At one event, I ended up talking to Robbie Fairbairn, one of the top executives at BlackRock. I told him how I owned my first stock at age 9 and how I started by IRA at age 15. We went on talking about investor education and it was a really fun conversation. At one point I mentioned how much I love Vanguard, to which he replied something along the lines of, "Ah Vanguard. What is it about them? They have such a massive and devoted following. Now how do we get iShares to have that!" (BlackRock owns iShares and aggressively competes with Vanguard in the ETF market). I remember thinking about that comment later that night. Both Vanguard and BlackRock have very inexpensive funds and make excellent ETF products, so why does Vanguard have such a loyal fan base? Could it be marketing? No, iShares does more marketing than Vanguard.

I realized it's because of how Vanguard is structured -- they created the company in such a way that the company values align directly with their investors' values. There is no separate "company" and "investor" -- they are one in the same. BlackRock on the other hand is a public company, and has a responsibility to return value to their shareholders in the form of profits. So while their funds may be as cheap or nearly as cheap as Vanguard's, which company makes it easier to trust them?